Principles Of Finance For My Auto loan

The major method dealers earn money is via a dealer-financed auto loan. Unlike a bank or cooperative credit union, cars and truck dealers generally aren’t direct lending institutions. They function as aggregators, matching your loan with one of their providing partners. With lots of various loan options to pick from, it is essential that you do your research before seeking funding for your next car and truck purchase.

It might seem like a longer-term loan is ideal because of the lower regular monthly payments. But look farther beyond short-term fulfillment if you can afford it in your month-to-month spending plan. It’s clear that cars and truck dealerships will undoubtedly give you a bunch of “bonus” like extended service warranties, rust-proofing, material protection, and security systems.

However, rolling them into your loan isn’t ideal because the interest shows that you will pay more for these additionals in the long run (How to find a car loan).

Lots of lenders will knock a bit off your rate if you register for automated payments or pay your costs online. Others might offer you a discount if you have a previous banking relationship with them or you’re buying a particular kind of car.

How To Find A Car Loan

You’re not going to find a 0% rate of interest deal at banks or cooperative credit unions, but you might find them provided at the car dealership by your automobile manufacturer’s lender.

It sounds too excellent to be real, however, if you have excellent credit you might have the ability to capture such a deal. https://www.youtube.com/embed/RUi5ObQy6GY

You ‘d need to do the math to determine which would save you more over the life of your loan. Anybody can get a vehicle loan. Even if you have no credit or a poor score, some lenders will prefer to deal with you. Lenders likewise look at the debt-to-income ratio, how long you have utilized at your existing company, and the details of the cars and truck you’re going to acquire.

If your credit is bad or you have no credit, you might not receive a bank loan. There are lenders who will provide to you if your credit is less than excellent, but bear in mind you might pay a greater rate of interest and loan terms may not be the best.

What Does Getting An Auto Loan Mean?

Your credit history is the single most important consideration for the rates of interest you’ll be provided. Outstanding credit will likely result in a low rate, and bad credit a high rate of interest (if you can certify at all).

Understanding your credit report ahead of time will assist you understand what kind of loan terms you can expect to certify.

We advise looking at deals from a couple of different loan providers and going to the dealership pre-approved. This is our exclusive scoring metric to compare services and products at The Basic Dollar in a transparent, evidence-based way. Our editorial team identifies 5 quantifiable elements to compare for each brand name, identifies the score requirements for each aspect score, then averages the five-element scores to produce a single Simple Score – Finding the best car loan.

Scores are a directional tool to assist in the procedure of picking an auto loan company. Be sure to continue your research and look around for the very best auto loan that fits your specific needs. We welcome your feedback on this short article and would love to find out about your experience with the car loans we advise.

An Unbiased View of Finding The Best Car Loan

Covid-19 pandemic has actually had a huge effect on the vehicle industry. According to Dino Selita, President of The Financial Obligation Relief Company, “Literally every dealership is currently offering 0% APR on automobile loans and most providing payment deferments.” Selita ensured us that, “A financing manager of the dealer has the power to get you a 0% rate of interest even if you do not certify!” If you’re acquiring a car during this time, do not hesitate to work out for the distinct terms offered today.

You might likewise have the ability to minimize your insurance premiums if you’re feeling the crunch of COVID-19 on your finances.

When looking for an automobile loan with a credit report varying between 700 and 709, you can expect to receive excellent rates of interest. At the same time, it’s still important to look around for the very best deals. Here’s a guide to vehicle loans for people in the 700 to 709 credit rating variety, together with tips for improving your credit report so you can certify for an even better rate next time around.

Guide For Getting The Best Rating

This type of rating puts you right at the average or somewhat above average amongst customers in the United States. For instance, If your rating dips any lower than around 670, nevertheless, you risk falling under “fair” territory, which is where you’ll see greater rates of interest.

By contrast, if your score to 750, you’re above average compared to other consumers, and your score is identified as “very great. “Simply put, a 700 credit history is solid, and you probably will not come across any difficulty receiving an automobile loan.

Rate of interest varies with the marketplace, so it’s an excellent idea to look for the very most current rates if you’re shopping around for a vehicle loan.

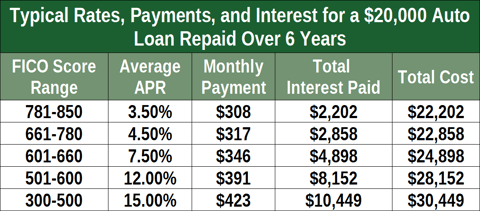

Automobile Loan Rates

According to U.S. News, the typical interest rates for automobile loans based upon credit history for individuals purchasing a brand-new vehicle in 2020 are as follows:

Exceptional (750+) 4.97%, Good (700-749) 5.04%, Fair (650-699) 11.89%, Poor (450-699) 18.85%, Really Bad (449 or lower) 20.11%. Individuals with ratings in the “extremely bad” variety may not certify for an automobile loan and will pay high rates of interest when they do.

U.S. Report likewise noted the 2020 car loan rate of interest for individuals buying a utilized vehicle. Outstanding (750+) 5.22%, Excellent (700-749) 5.29%, Fair (650-699) 12.14%, Poor (450-699) 19.10%, Really Bad (449 or lower) 20.36%. Remember that these are simply averages. Depending on your individual scenarios, such as your income if any, you put down, you could qualify for greater or lower rates of interest.

What Does Finance For My Auto Do?

In basic, cooperative credit unions tend to provide lower rates of interest than banks. Unlike banks, credit unions are owned by their members, which means they have an incentive to keep rates as low as possible.

A drawback of financing through a cooperative credit union is that you must be a member to get a car loan. Assuming you get approved for subscription, Consumers Cooperative credit unions are known for providing vehicle loan rates of interest well below the national average.

Among the good features of Consumers Credit Union, you do not need to be part of a particular group or market to sign up with. While numerous credit unions cater exclusively to teachers, firemen, or other groups. Customers Credit Union is open to anyone who pays the $5 subscription and has a minimum 640 credit history.

Through its Vehicle Navigator tool, Capital One lets you prequalify for a vehicle loan, so you know your funding terms and rate of interest before you purchase a vehicle. Capital One won’t do a tough pull of your credit report if you get pre-qualified, so there’s no risk in using the Vehicle Navigator tool.